The semiconductor industry is one of the most pivotal sectors in today’s tech-driven world. From powering the latest smartphones and laptops to enabling advancements in artificial intelligence and autonomous vehicles, semiconductors are the backbone of nearly all modern technology. At the heart of this industry lies the semiconductor foundries—companies that specialize in manufacturing chips designed by other firms.

The semiconductor industry is poised for another transformative year in 2025. Following a year of record-breaking growth in AI-related semiconductors and notable struggles in legacy sectors, the landscape is set for both challenges and opportunities. For investors and financial advisors, understanding these dynamics is crucial to navigating the road ahead.

In 2025, the competition among semiconductor foundries is fierce, with technological advancements and massive investments driving innovation. Below, we explore the top 10 semiconductor foundries in the world, comparing their market positions, technologies, and capabilities.

| Rank | Foundry Name | Revenue (2024) | Market Share | Process Technology | Key Clients |

|---|---|---|---|---|---|

| 1 | TSMC (Taiwan Semiconductor Manufacturing) | $79.8 Billion | 56% | 3nm, 5nm, 7nm, 10nm | Apple, AMD, Nvidia, Qualcomm |

| 2 | Samsung Foundry | $30.1 Billion | 19% | 3nm, 5nm, 7nm | Qualcomm, IBM, Nvidia, Intel |

| 3 | GlobalFoundries | $25.7 Billion | 8.3% | 12nm, 14nm, 22nm | AMD, Qualcomm, Broadcom, NXP |

| 4 | SMIC (Semiconductor Manufacturing International Corporation) | $7.2 Billion | 5.5% | 7nm, 14nm, 28nm | Huawei, MediaTek, Unisoc |

| 5 | UMC (United Microelectronics Corporation) | $6.7 Billion | 5% | 28nm, 40nm, 55nm | Broadcom, MediaTek, Intel |

| 6 | Intel Foundry Services (IFS) | $4.5 Billion | 3.5% | 5nm, 7nm, 10nm | Qualcomm, Amazon, Apple (planned) |

| 7 | Powerchip Technology | $3.6 Billion | 2.5% | 28nm, 40nm | Micron, Nanya Technology, Inotera |

| 8 | TSMC (Joint Ventures) | $2.9 Billion | 1.5% | 28nm, 45nm | Broadcom, Intel |

| 9 | Vanguard International Semiconductor | $2 | / | / | / |

1. TSMC (Taiwan Semiconductor Manufacturing Company)

Headquarters: Taiwan

Revenue (2024): $79.8 Billion

Market Share: 56%

Process Technology: 3nm, 5nm, 7nm, 10nm

Key Clients: Apple, AMD, Nvidia, Qualcomm

TSMC continues to dominate the semiconductor foundry landscape in 2025, holding a commanding market share of over 50%. Known for its cutting-edge process technologies, TSMC’s 3nm node is the latest breakthrough in semiconductor manufacturing, offering superior performance and power efficiency. The company invests heavily in R&D to maintain its lead in advanced manufacturing processes. Its clientele includes the world’s largest tech companies, including Apple, AMD, and Nvidia.

2. Samsung Foundry

Headquarters: South Korea

Revenue (2024): $30.1 Billion

Market Share: 19%

Process Technology: 3nm, 5nm, 7nm

Key Clients: Qualcomm, IBM, Nvidia, Intel

Samsung Foundry is TSMC’s main competitor in the high-performance semiconductor market. With a focus on memory and logic chip manufacturing, Samsung has heavily invested in EUV (Extreme Ultraviolet) lithography to keep pace with TSMC's advancements. Samsung’s 3nm process technology, which utilizes Gate-All-Around (GAA) transistors, offers a leap in performance and energy efficiency.

3. GlobalFoundries

Headquarters: USA

Revenue (2024): $25.7 Billion

Market Share: 8.3%

Process Technology: 12nm, 14nm, 22nm, 28nm

Key Clients: AMD, Qualcomm, Broadcom, NXP

GlobalFoundries, based in the United States, is a key player in the semiconductor foundry market, although it lags behind TSMC and Samsung in terms of advanced nodes. Specializing in mature process technologies, GlobalFoundries is a crucial supplier for automotive, industrial, and consumer electronics sectors. The company is known for its reliability and scalability, particularly for legacy node production.

4. SMIC (Semiconductor Manufacturing International Corporation)

Headquarters: China

Revenue (2024): $7.2 Billion

Market Share: 5.5%

Process Technology: 7nm, 14nm, 28nm

Key Clients: Huawei, MediaTek, Unisoc

SMIC, China’s largest foundry, has made significant strides in narrowing the technological gap with global leaders. Although still behind TSMC and Samsung in cutting-edge process technology, SMIC is a key player in the production of 7nm and 14nm chips. It is the primary foundry partner for domestic tech giants like Huawei and MediaTek, despite facing restrictions on advanced equipment due to geopolitical tensions.

5. UMC (United Microelectronics Corporation)

Headquarters: Taiwan

Revenue (2024): $6.7 Billion

Market Share: 5%

Process Technology: 28nm, 40nm, 55nm

Key Clients: Broadcom, MediaTek, Intel

United Microelectronics Corporation (UMC) is one of Taiwan's leading semiconductor foundries, specializing in mature and specialty nodes. UMC provides a reliable supply of chips for automotive, consumer electronics, and industrial applications. Although it lags behind the leading foundries in advanced process technology, UMC is a strong contender in the mid-range to mature semiconductor nodes.

6. Intel Foundry Services (IFS)

Headquarters: USA

Revenue (2024): $4.5 Billion

Market Share: 3.5%

Process Technology: 5nm (planned), 7nm, 10nm

Key Clients: Qualcomm, Amazon, Apple (planned)

Intel has historically been a leading chip designer and manufacturer for its own products. However, its entry into the foundry business is relatively new, with Intel Foundry Services (IFS) launched as part of a strategy to regain market share in semiconductor manufacturing. Intel is expected to lead in advanced process technologies, including 5nm nodes, in the coming years, which will allow it to attract more customers like Qualcomm and Amazon.

7. Powerchip Technology

Headquarters: Taiwan

Revenue (2024): $3.6 Billion

Market Share: 2.5%

Process Technology: 28nm, 40nm

Key Clients: Micron, Nanya Technology, Inotera

Powerchip Technology focuses primarily on DRAM and flash memory production, as well as CMOS image sensors. It plays an important role in memory semiconductor manufacturing but is not a major player in logic IC production. Powerchip serves customers primarily in the memory space, including major players like Micron.

8. Taiwan Semiconductor Manufacturing Company (TSMC) - Joint Ventures

Headquarters: Taiwan

Revenue (2024): $2.9 Billion

Market Share: 1.5%

Process Technology: 28nm, 45nm

Key Clients: Broadcom, Intel

TSMC has a number of joint ventures and strategic alliances that enable it to further consolidate its market position. These ventures help expand TSMC's capacity in specialized and niche semiconductor markets, particularly in the automotive and IoT sectors.

9. Vanguard International Semiconductor

Headquarters: Taiwan

Revenue (2024): $2.4 Billion

Market Share: 1.2%

Process Technology: 0.18μm, 0.25μm

Key Clients: NXP, Qualcomm

Vanguard International Semiconductor is a key player in the low- to mid-range semiconductor node market. While it does not compete with the leaders in the high-performance segment, it is a reliable source for mature semiconductor processes, catering to a wide range of industries such as automotive, medical devices, and consumer electronics.

10. DB HiTek

Headquarters: South Korea

Revenue (2024): $1.7 Billion

Market Share: 0.9%

Process Technology: 28nm, 65nm

Key Clients: LG Electronics, Samsung Electronics

DB HiTek is a relatively small player in the semiconductor foundry industry, focusing primarily on analog and mixed-signal semiconductor production. While it doesn’t compete in the advanced logic node market, it provides specialized solutions for automotive, industrial, and consumer markets.

Undervalued Players Emerging

While market leaders grab headlines, undervalued players in memory chips and semiconductor equipment offer attractive opportunities for strategic positioning. Companies like SK Hynix and Micron are poised for growth as the memory market stabilizes, driven by stronger customer relationships and a shift toward contract-based demand. SK Hynix is positioned to benefit from demand for high-bandwidth memory (HBM), which is increasingly vital for AI applications. Western Digital, though less concentrated in HBM, also offers a potential upside as the market stabilizes.

On the equipment side, Applied Materials and Lam Research stand out as key beneficiaries of industry demand cycles, offering compelling value. With improving fundamentals and strategic alignment with future technology trends, these companies represent critical enablers of the semiconductor ecosystem. Emerging players like Onto Innovation and ACMR Technologies also present intriguing growth stories as their innovative solutions gain traction in the broader market.

Key Takeaways for the Semiconductor Market in 2025

1. Stay Aligned with AI: Market leaders like Nvidia, Marvell, and TSMC are set to remain at the forefront of AI growth. Keep an eye on developments in hyperscaler-driven chip alternatives, including Broadcom and AMD.

2. Watch for Recovery: Automotive, IoT, and analog sectors may rebound, offering potential upside for diversified portfolios. Companies like Texas Instruments and Analog Devices could see improvement in these segments.

3. Explore Hidden Value: Memory chips (SK Hynix, Micron, Western Digital) and semiconductor equipment (Applied Materials, Lam Research, Onto Innovation) represent undervalued opportunities.

4. Monitor Fragmentation Risks: The increasing diversity in AI solutions could create competitive pressures but also open doors for new players and technologies.

5. Stay Vigilant: Inventory challenges and cyclical risks require careful monitoring, even as growth prospects remain strong.

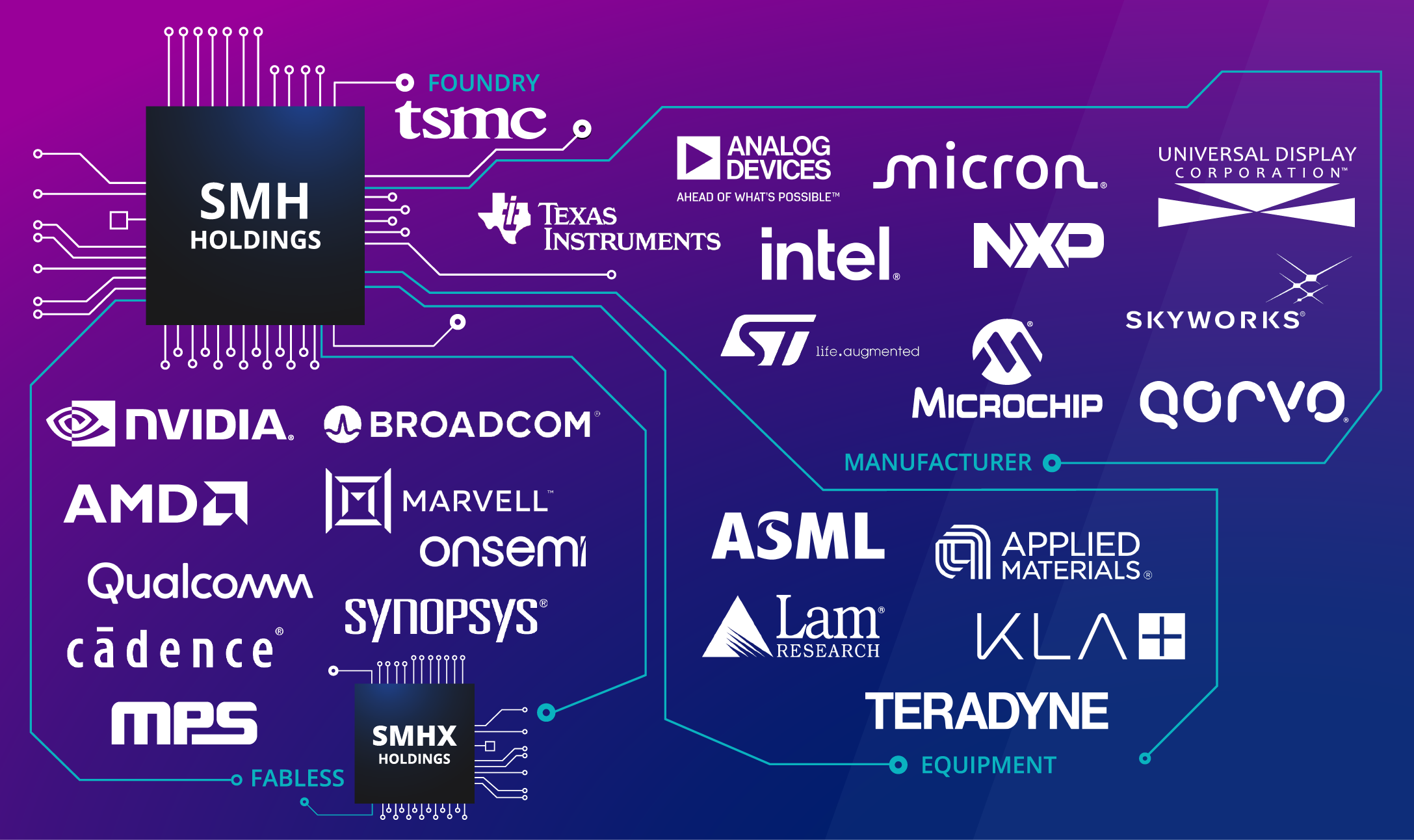

A Roadmap for Semiconductor Investors

For those investing in the semiconductor space, 2025 is a year to remain forward-looking yet cautious. The industry’s evolution, driven by AI and emerging technologies, creates a fertile ground for growth while demanding strategic positioning. ETFs like the VanEck Semiconductor ETF (SMH) and the VanEck Fabless Semiconductor ETF (SMHX) offer diversified exposure to both leading innovators and emerging players, making them valuable tools for navigating this dynamic sector.

As we move through 2025, staying informed and adaptable will be key to capitalizing on the opportunities this pivotal industry presents. The semiconductor story is far from over—and this year may be one of its most exciting chapters yet.

Written by Icey Ye from AIChipLink.

AIChipLink, one of the fastest-growing global independent electronic component distributors in the world, offers millions of products from thousands of manufacturers. Whether you need assistance finding the right part or electronic components manufacturers for your design, you can contact us via phone, chat or e-mail. Our support team will answer your inquiries within 24 hours.

Disclaimer: This article is provided for general information and reference purposes only. The opinions, beliefs, and viewpoints expressed by the author of this article do not necessarily reflect the opinions, beliefs, and viewpoints of AIChipLink or official policies of AIChipLink.